For many Nepalese businesses, Tax Deducted at Source (TDS) feels routine. A percentage is deducted, deposited, and forgotten. It rarely receives the same attention as VAT or income tax. And that is exactly why it has quietly become one of the most expensive compliance blind spots in Nepal.

According to data released by the Inland Revenue Department and reported by Khabarhub, A total of 193,620 taxpayers owe Rs 219.11 billion in income tax, a significant portion of which is linked to incorrect withholding and TDS mismatches. This shows that TDS errors are systemic compliance weaknesses, not just clerical mistakes.

For IT companies, outsourcing firms, consultants, and service exporters, TDS mistakes are even more dangerous. These businesses rely heavily on contractors, freelancers, service vendors, foreign payments, and mixed income streams. Each of these carries TDS implications that are often misunderstood or applied incorrectly.

Why TDS Is So Commonly Mismanaged in Nepal

TDS laws in Nepal are detailed and situational. The TDS rate depends on the nature of payment, the status of the recipient, and whether the transaction is local or foreign. Many business owners assume that once they deduct something, they are safe. In reality, incorrect deduction can be just as risky as no deduction at all.

One major reason TDS mistakes persist is that responsibility is fragmented. Business owners focus on operations. Accountants focus on entries. Compliance often falls in between. When no one fully owns the process, small errors go unnoticed.

Another reason is that TDS rules evolve. Rates, thresholds, and classifications change through Finance Acts and IRD directives. Businesses that rely on past practice rather than current regulation continue repeating outdated methods.

Many firms still rely on informal knowledge or peer advice for tax compliance instead of updated legal guidance. This creates consistency in mistakes. When everyone follows the same wrong practice, it feels normal until enforcement begins.

The Hidden Cost of Incorrect TDS Deduction

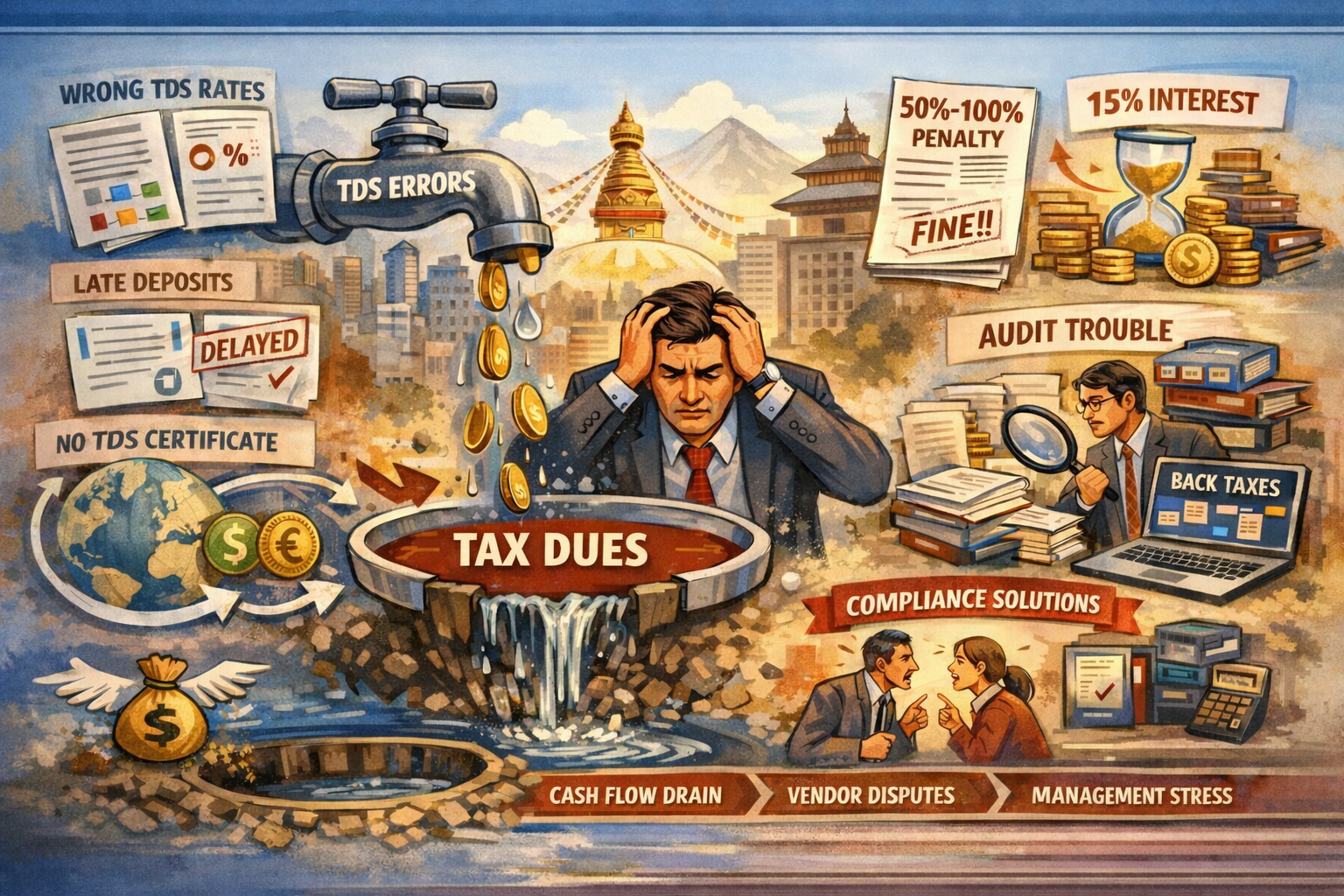

The most dangerous aspect of TDS mistakes is that the cost is rarely immediate. The financial drain happens quietly over time. Below are the breakdown of fines and penalties in case of TDS non-compliance according to Income Tax Act, (2058):

Penalties for Incorrect Statements:

- Unintentional/Mistaken Error: If a false or misleading statement is made unintentionally, the penalty is 50% of the amount of tax short paid, Section (120).

- Intentional Error/False Return: If a false or misleading statement is made knowingly or recklessly, the penalty is 100% of the amount of tax short paid, Section (120).

Late Filing of Return:

- For failing to file a TDS return by the due date, interest of 15% p.a. on any unpaid amount along Rs 1000 monthly, Section (117).

Failing to Maintain Proper Documentation:

- For failing to have a proper record of the tax details, a fine of Rs. 100 per month or 0.1% p.a. on accessible income whichever is higher, Section (117).

Failing to Comply with Provisions:

- For failing to follow the Income Tax Act provisions, liable to pay rs.5000 to rs.25000, Section (119(ka)).

In short, TDS errors do not just create tax problems. They disrupt cash flow, strain partnerships, and consume management time.

Why IT and Service Companies Are More Exposed

IT firms and service exporters operate with payment structures that are TDS-intensive. Monthly contractor payments, consultant fees, professional services, digital subscriptions, foreign remittances, and commission-based payouts all carry withholding implications.

A Kathmandu Valley tech firm specializing in outsourced digital solutions recently underwent an audit triggered by the inconsistent application of TDS (Tax Deducted at Source) for its freelancers. Because these freelancers worked full-time, the firm’s records showed contradictory treatment: payments were sometimes mistakenly categorized as employee salaries with full TDS slab rates, and other times correctly as service providers with the lower professional rate, or occasionally, no TDS was withheld.

When the IRD reviewed the books, this hybrid, contradictory treatment resulted in a major compliance failure. Although the payments were genuine, the inconsistency led to substantial backdated penalties: Late Payment Interest 15% along with Rs 1000 monthly additional fine, incorrect deductions penalty 50% if the inaccuracy is unintentional or 100% for intentionally filing incorrect tax, Income Act (2058).

Common TDS Mistakes Nepalese Businesses Make

One of the most frequent mistakes is applying a flat TDS rate to all payments without understanding the nature of the expense while another is delaying TDS deposit beyond the deadline, assuming it can be adjusted later.

Many firms deduct TDS but fail to issue certificates on time, creating reconciliation issues for vendors. Others deduct TDS on payments that are exempt or apply withholding where it is not required, leading to unnecessary disputes.

Foreign payments are another area of confusion. Payments for software subscriptions, cloud services, or foreign consultants often trigger withholding obligations that businesses overlook entirely.

These mistakes are rarely intentional. They happen because TDS is treated as a mechanical step, not a compliance system that requires design and oversight.

TDS as a Control System: How Smart Companies Manage Compliance

Well-run businesses treat TDS as a continuous control system, not a monthly calculation. They focus on proper vendor classification, clear payment categorization, correct rate mapping, documented agreements, and regular monthly reconciliation. This disciplined approach reduces audit risk, keeps expenses deductible, preserves vendor trust, and supports stable cash flow.

In Nepal’s tightening compliance environment, where IRD increasingly cross-checks TDS deposits with income declarations and vendor filings, this level of control is becoming essential.

As a result, many companies especially in IT, consulting, and export services are moving away from fragmented handling. They rely on specialists for ongoing compliance, timely deposits, and audit-ready records. They are outsourcing withholding compliance to specialists who understand both the law and the business model. These companies understand that TDS is not about saving tax. It is about avoiding unnecessary loss.

How KBC Helps Businesses Stop TDS Leakages

At Kathmandu Business Consultants, we help businesses identify and eliminate TDS inefficiencies before they turn into liabilities. We start by reviewing your payment structures, vendor agreements, contractor arrangements, and historical deductions.

We identify where rates are misapplied, where deposits are delayed, and where documentation is weak. We then design a TDS framework tailored to your business model, not a generic checklist.

Each month, we manage deductions, deposits, certificates, and reconciliation. We ensure that expenses remain deductible, vendors remain satisfied, and audits remain manageable.

For IT and service-based companies, we pay special attention to contractor payments, foreign services, subscription expenses, and cross-border transactions where TDS mistakes are most common. Our focus is simple. We stop silent financial drain before it becomes a visible problem.

Conclusion: Turn TDS from a Risk into a Competitive Advantage

In Nepal, TDS remains one of the most overlooked sources of business loss. It rarely attracts attention like VAT suspensions or tax raids, yet it steadily erodes cash flow, consumes management time, and strains vendor relationships.

Companies that treat TDS as an afterthought will keep absorbing avoidable penalties and disallowed expenses. Those that manage it with structure and foresight protect margins, stay audit-ready, and operate with confidence in a tightening compliance landscape.

TDS is not just a deduction. It is a discipline. With the right systems and the right compliance partner, it becomes a source of control, not stress.

Leave a Reply